How Equity Release Mortgages Work with Inheritance Planning

The Crucial Elements to Consider Prior To Making An Application For Equity Release Mortgages

Before getting equity Release home mortgages, people need to meticulously take into consideration numerous crucial factors. Understanding the implications on their financial scenario is crucial. This includes evaluating present revenue, prospective future expenses, and the effect on inheritance. In addition, checking out numerous product types and connected costs is important. As one navigates these complexities, it's crucial to evaluate emotional connections to property versus useful financial requirements. What various other considerations might affect this considerable decision?

Understanding Equity Release: What It Is and Just how It Works

Equity Release allows home owners, generally those aged 55 and over, to access the wealth linked up in their residential property without requiring to market it. This monetary solution makes it possible for individuals to reveal a part of their home's value, giving cash that can be made use of for various objectives, such as home improvements, financial debt repayment, or improving retired life income. There are two major kinds of equity Release items: lifetime home mortgages and home reversion strategies. With a lifetime home mortgage, property owners retain ownership while obtaining versus the residential or commercial property, settling the car loan and rate of interest upon fatality or relocating right into long-term care. On the other hand, home reversion entails marketing a share of the home in exchange for a swelling amount, allowing the property owner to stay in the home till death. It is essential for prospective applicants to comprehend the ramifications of equity Release, consisting of the effect on inheritance and possible costs related to the setups.

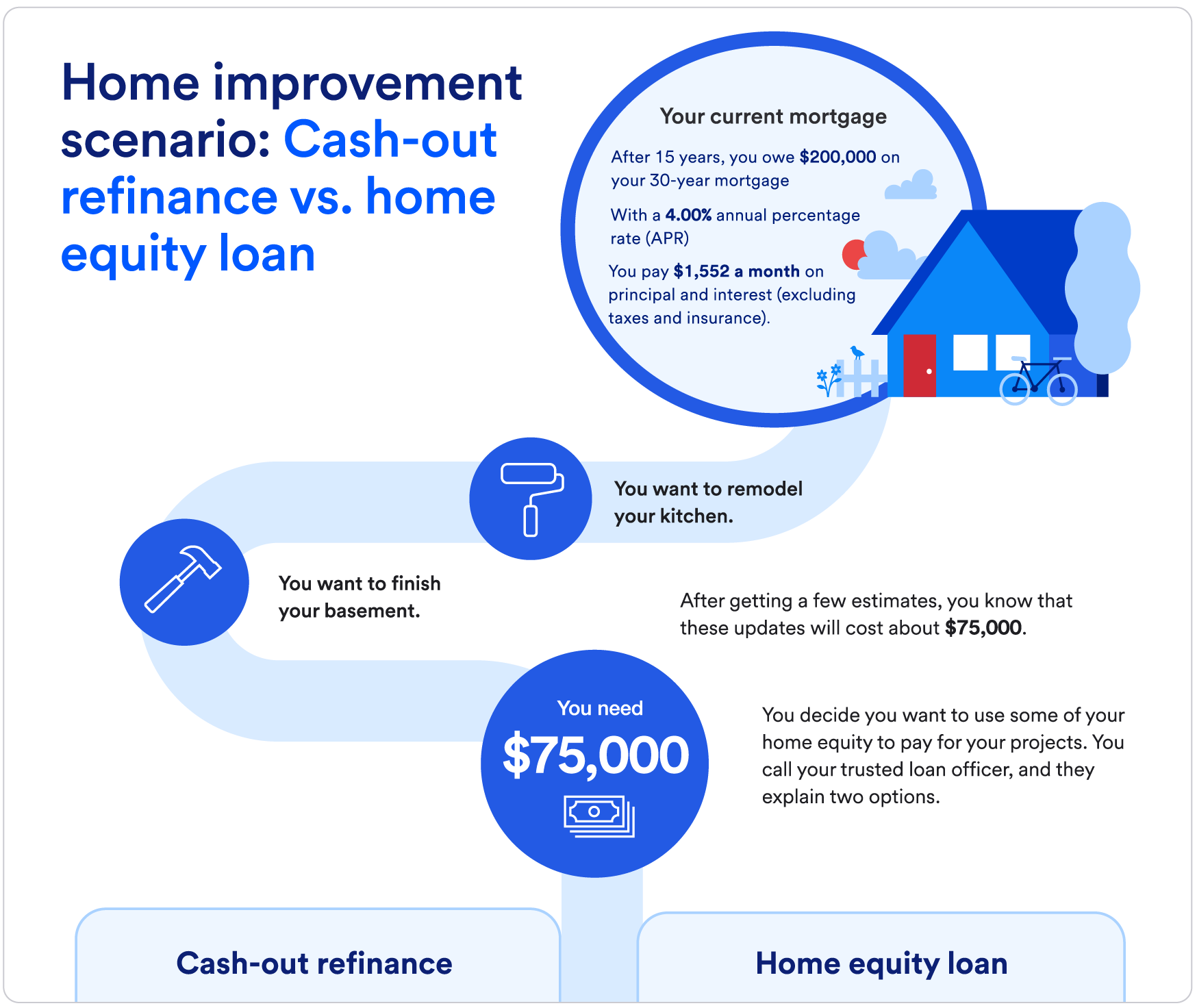

:max_bytes(150000):strip_icc()/homeequityloan-e11896bf4ac1475a9806a55f92e0c312.jpg)

Evaluating Your Financial Scenario and Future Demands

Just how can a homeowner successfully review their economic situation and future requirements prior to thinking about equity Release? First, they need to carry out a comprehensive analysis of their present revenue, expenditures, and savings. This includes evaluating monthly bills, existing debts, and any prospective revenue sources, such as investments or pensions. Comprehending money circulation can highlight whether equity Release is essential for economic stability.Next, property owners should consider their future needs. This involves anticipating possible medical care prices, way of living adjustments, and any kind of significant expenditures that might develop in retirement. Establishing a clear budget plan can help in determining exactly how much equity may be needed.Additionally, seeking advice from an economic expert can supply insights into the lasting implications of equity Release. They can assist in aligning the property owner's economic scenario with their future objectives, guaranteeing that any kind of decision made is informed and aligned with their total financial health.

The Effect on Inheritance and Household Finances

The choice to make use of equity Release home loans can considerably affect household funds and inheritance planning. Individuals need to consider the effects of inheritance tax obligation and how equity distribution among beneficiaries may change therefore. These aspects can affect not only the financial heritage left but additionally the relationships amongst household participants.

Estate Tax Implications

Several homeowners think about equity Release home mortgages as a method to supplement retired life earnings, they might accidentally affect inheritance tax liabilities, which can significantly influence family financial resources. When property owners Release equity from their property, the amount obtained plus rate of interest collects, reducing the worth of the estate left to heirs. This could lead to a higher inheritance tax expense if the estate surpasses the tax obligation threshold. Furthermore, any type of continuing to be equity might be regarded as component of the estate, making complex the financial landscape for recipients. Family members have to be aware that the choice to accessibility equity can have lasting effects, possibly lessening the inheritance planned for liked ones. As a result, cautious consideration of the implications is necessary before continuing with equity Release.

Family Members Financial Planning

While taking into consideration equity Release mortgages, family members must acknowledge the significant influence these financial decisions can have on inheritance and overall family financial resources. By accessing home equity, property owners might minimize the value of their estate, possibly impacting the inheritance left to heirs. This can bring about feelings of unpredictability or conflict among household members pertaining to future monetary assumptions. Additionally, the costs linked with equity Release, such as rate of interest and costs, can collect, decreasing the continuing to be properties offered for inheritance. It is crucial for households to take part in open discussions regarding these issues, making sure that all members recognize the effects of equity Release on their long-term financial landscape. Thoughtful planning is vital to stabilize prompt economic requirements with future household legacies.

Equity Distribution Amongst Successors

Equity circulation among beneficiaries can substantially change the financial landscape of a family members, especially when equity Release mortgages are entailed. When a homeowner makes a decision to Release equity, the funds drawn out may reduce the estate's general value, affecting what heirs obtain. This reduction can cause disagreements amongst member of the family, specifically if assumptions pertaining to inheritance vary. The responsibilities tied to the equity Release, such as settlement terms and interest accumulation, can make complex monetary planning for successors. Family members need to take into consideration exactly how these aspects influence their long-term financial health and relationships. Seminar regarding equity Release decisions and their implications can assist ensure a clearer understanding of inheritance dynamics and mitigate potential problems amongst successors.

Exploring Various Sorts Of Equity Release Products

When taking into consideration equity Release choices, individuals can select from numerous distinctive items, each tailored to various economic requirements and conditions. One of the most typical types consist of life time home loans and home reversion plans.Lifetime mortgages permit house owners to borrow versus their property worth while keeping possession. The financing, in addition to accumulated passion, is paid back upon the homeowner's fatality or when they relocate into long-term care.In contrast, home reversion plans entail offering a portion of the home to a provider in exchange for a round figure or normal payments. The home owner can continue residing in the company website residential property rent-free until death or relocation.Additionally, some items use flexible functions, enabling consumers to withdraw funds as needed. Each item lugs distinct benefits and factors to consider, making it necessary for people to assess their monetary goals and lasting implications before selecting one of the most suitable equity Release alternative.

The Duty of Interest Rates and Fees

Picking the appropriate equity Release item involves an understanding of different financial elements, consisting of rates of interest and associated charges. Passion prices can greatly affect the general price of the equity Release strategy, as they establish exactly how much the consumer will certainly owe over time. Fixed rates use predictability, while variable rates can change, impacting long-lasting monetary planning.Additionally, customers must be mindful of any upfront charges, such as setup or appraisal charges, which can contribute to the first price of the home mortgage. Continuous charges, including annual monitoring fees, can likewise collect over the regard to the finance, possibly reducing the equity offered in the property.Understanding these expenses is vital for debtors to evaluate the complete monetary commitment and ensure the equity Release product straightens with their economic objectives. Cautious consideration of rate of interest and fees can help individuals make informed choices that match their scenarios.

Seeking Professional Advice: Why It is necessary

Just how can individuals navigate the intricacies of equity Release home loans efficiently? Seeking professional advice is a crucial action in this procedure. Financial consultants and home loan brokers have specialized understanding that can brighten the ins and outs of equity Release items. They can provide customized assistance based upon a person's distinct monetary situation, making certain educated decision-making. Experts can aid clear up problems and terms, identify prospective challenges, and highlight the long-lasting ramifications of getting in into an equity Release arrangement. In addition, they can assist in contrasting various choices, making sure that individuals choose a plan that aligns with their objectives and demands.

Evaluating Alternatives to Equity Release Mortgages

When considering equity check out this site Release home loans, people may find it valuable to explore various other funding options that might better match their demands. This consists of assessing the possibility of downsizing to accessibility resources while preserving monetary security. A comprehensive analysis of these choices can lead to more educated choices regarding one's financial future.

Other Financing Options

Downsizing Considerations

Downsizing offers a feasible alternative for individuals browse around this web-site taking into consideration equity Release home loans, particularly for those seeking to access the worth of their residential or commercial property without sustaining extra debt. By selling their present home and purchasing a smaller, much more inexpensive property, house owners can Release considerable equity while reducing living expenditures. This choice not only reduces financial concerns yet likewise streamlines maintenance responsibilities linked with larger homes. Furthermore, scaling down may give a possibility to transfer to a preferred location or a neighborhood customized to their way of life requires. Nevertheless, it is essential for individuals to evaluate the psychological facets of leaving a long-time home, as well as the possible costs associated with relocating. Cautious factor to consider of these factors can cause a much more gratifying monetary choice.

Often Asked Inquiries

Can I Still Move Residence After Obtaining Equity Release?

The person can still relocate home after securing equity Release, yet they have to assure the new building fulfills the lending institution's requirements (equity release mortgages). In addition, they might need to pay back the loan upon moving

What Happens if My Residential Or Commercial Property Value Decreases?

The house owner may encounter lowered equity if a property's worth reduces after taking out equity Release. However, lots of plans use a no-negative-equity assurance, guaranteeing that repayment quantities do not go beyond the building's value at sale.

Exist Age Restrictions for Equity Release Candidates?

Age restrictions for equity Release applicants typically need individuals to be a minimum of 55 or 60 years old, relying on the service provider. These criteria guarantee that candidates are likely to have sufficient equity in their residential or commercial property.

Will Equity Release Impact My Qualification for State Benefits?

Equity Release can possibly influence eligibility for state advantages, as the launched funds may be taken into consideration income or capital (equity release mortgages). Individuals need to speak with economic advisors to comprehend how equity Release impacts their certain benefit privileges

Can I Settle the Equity Release Mortgage Early Without Penalties?

Final thought

In recap, navigating through the intricacies of equity Release home mortgages calls for mindful factor to consider of various aspects, including economic scenarios, future requirements, and the potential effect on inheritance. Comprehending the various product options, connected prices, and the relevance of specialist support is necessary for making notified decisions. By completely assessing options and stabilizing emotional attachments to one's home with practical monetary requirements, people can identify one of the most suitable approach to accessing their home equity sensibly (equity release mortgages). Developing a clear budget can assist in figuring out exactly how much equity might be needed.Additionally, consulting with a financial consultant can give insights into the long-term effects of equity Release. Equity circulation amongst heirs can significantly change the financial landscape of a family members, especially when equity Release home loans are involved. Ongoing charges, consisting of annual administration fees, can additionally collect over the term of the loan, potentially lowering the equity available in the property.Understanding these expenses is vital for debtors to review the complete monetary dedication and ensure the equity Release item aligns with their economic goals. If a building's value decreases after taking out equity Release, the property owner may encounter minimized equity. Equity Release can possibly influence eligibility for state benefits, as the launched funds may be thought about income or funding